Market review

The easing in US headline inflation has given investors confidence that central banks are likely to slow the pace of rate hikes in 2023. This has brought a calm to bond markets. While corporate earnings continue to weaken, in-line with a slowing economic backdrop, lower volatility in bond markets helped equities climb in October and November. Quarter-to-date world equities are up 7.7% reducing the year-to-date loss to -2.3% (returns are measured in GBP). European and UK equities have outperformed other regions so far in Q4. Chinese equities also rallied recently as Beijing has signalled a relaxation in Covid controls. This has lifted broader Emerging Market equities. Government bonds have also risen (with yields coming down) and credit markets have benefited from lower yields and some tightening of spreads. (‘Spreads’ are the difference in the interest paid by a government bond vs. a corporate bond.) For sterling investors in overseas markets some of the gains have been offset by a stronger pound vs the dollar. The dollar has weakened in Q4.

Outlook

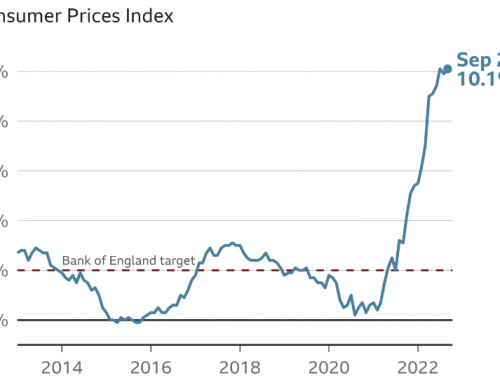

Higher interest rates will weaken demand for goods and services, by raising costs for consumers and companies. The idea is that with lower demand, prices will fall, thereby reducing inflation. We think there will be a recession in 2023 (if we’re not there already). Unlike previous recessions however, the economic slowdown has been well flagged. Both stocks and bonds have fallen in 2022 to reflect the impeding recession. We believe that while next year will be tough for economies and households, asset prices are looking attractive.

Inflation remains significantly above central bank targets, but that’s because there is a lag in higher interest rates impacting inflation and economic growth. Growth will continue to slow even if central banks slow the pace of rate hikes. The key question for investors is how much of the economic damage is already priced.

We think there is more damage to price into equities. Unlike previous periods of slowing growth, we don’t think central banks will start cutting rates which would otherwise support valuations. We have a neutral view on equities heading into next year.

On bonds, we think investment grade credit is attractively priced today. Higher yields and strong balance sheets mean that high quality corporate bonds will be better placed than equities to weather a slowing economy in 2023.

The higher rate environment presents both opportunities and risks. Fixed income finally offers yield and an option for investors having been starved of receiving income. We think rates will remain at a higher level than we’ve seen in the past decade. Previously, government bonds have shielded portfolios from recessions. That may not be the case in the future. A higher rate environment will require more dynamic asset allocation within multi-asset portfolios.