The first quarter of the year was a difficult environment for investors and this has persisted through April and May. The Russia-Ukraine conflict has continued, Food and energy prices remain high, Lockdowns in China and the prospect of tighter US monetary policy have all weighed on sentiment.

Global stock markets fell with the US stock market leading the way lower. Year-to-date the S&P 500 Index is down 12.8% (as of 31st May). In the UK, a large weighting to the energy sector continued to benefit UK equities, with the FTSE All Share Index up 1.5%. The FTSE All Share Index remains the only major equity market with positive returns year to date (local currency terms). European equities, represented by the Euro Stoxx 50 Index continue to struggle, down -9.6%. The impact on energy markets remains prominent given the difficulties faced by Europe in reducing its energy dependency on Russia.

Emerging market (EM) equities have so far recorded a negative return of 11.7%, represented by the MSCI Emerging Market Index. In fixed income, bonds lost ground as yields continued to rise (yields and prices move in opposite directions). Corporate bonds have been the worst performing fixed income segment year-to-date, in large part because of their sensitivity to interest rate movements. High yield saw the more significant spread widening though spreads remained below the highs seen earlier this year. (Investment grade bonds are the highest quality bonds as determined by a credit rating agency. High yield bonds are more speculative, with a credit rating below investment grade). The spread is the difference between the yield on a corporate bond and a government bond. Emerging market (EM) bonds also saw negative returns , particularly sovereign debt, while corporate credit was more resilient. Year-to-date, Emerging market debt represented by the JP Morgan Emerging Market Bond Index is down 14%.

Europe saw a continued rise in inflation and speculation around monetary tightening. European Central Bank President Christine Lagarde indicated that the first interest rate rise could potentially come this year, saying rates would rise after asset purchases had concluded. Data showed annual eurozone CPI inflation rise to 7.5% (year-on-year) in April, up from 7.4% in March.

Having kept Covid-19 under tight control for most of the past two years, the latest round of Omicron outbreaks in China is putting a brake on economic growth, especially in consumption and investment. While there is a growing expectation that the People’s Bank of China and the government should respond with aggressive economic stimulus to support the economy, the measures announced thus far have been more conservative than expected. Stock markets came under further pressure; year-to-date the MSCI China index is down 18%. Valuations on Chinese stocks relative to developed markets now stand at levels last seen in 2015.

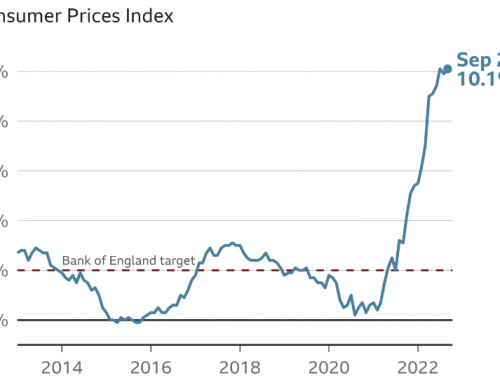

Central bank policy and geopolitics are key risks that investors will be watching closely. Markets would normally look at policy support to ease the pain. This time round, sky high inflation (US consumer price inflation accelerated to 8.3% year-on-year in April) is leaving central banks little choice but to maintain their plans to continue tightening. After implementing its first back-to-back interest rate hikes since 2006, the US Federal Reserve Chair Jerome Powell announced it will begin its balance sheet ($8.9 trillion) runoff in June in a step up in the central bank’s inflationary countermeasures. Market expectations are now calling for the Fed funds rate to zoom up to a peak around 3% over the next year, more than doubling since the start of the year. Therefore, investors have little reason to remain optimistic, which has reflected in price action this year.

Monetary policy tightening impacts global financial markets because when interest rates are higher, this increases the rate at which companies future cash flows are discounted. This results in lower valuations for equities.

Outlook

Central banks continue to cement their hawkish stance, but have a difficult balancing act in managing a slowdown in demand amidst a less optimistic economic outlook and disappointing macroeconomic data. We believe higher inflation will continue to impact returns on bonds while a slowdown in the global economy will likely drag equities lower.

Market pricing of inflation suggests an expectation that inflation will fall back eventually, but the key question is whether the swift withdrawal of stimulus will dent economic growth prospects, triggering a recession. This is complicated by the economic side effects of the continuing Russia-Ukraine conflict, with it having a material impact on inflation and supply chains that had already been hit by the COVID crisis.