Market review

Q3 was a positive quarter for equities; following on from increases in both Q1 and Q2. In the UK the FTSE All Share rose by 2.2%; while in the US the S&P 500 rose 3.1% in sterling terms. Europe was relatively flat in comparison, only rising by 0.7%. The best performing market in sterling terms though this quarter was Japan, where the Topix rose 7.3%. The weak area was the Emerging Markets, which saw a sell off with a decline of 4.3%.

Concerns about inflation and the future direction of interest rates caused a decline in the UK gilt markets, with the All Gilts Index falling by 1.8% and Corporate bonds down -1.0%. Only Indexed Linked Gilts gave a positive return, which was 2.3%.

The pace of economic growth is now declining (not stalling but the rate of growth is not as high as it has been in the Covid “bounce-back” period). But consumers are likely to want to spend some of their accumulated savings in coming months; plus companies are trying to build their inventories and governments are still trying to support the economic cycle through quantitative easing programmes, infrastructure projects and other investments. This is likely to cause economic growth to remain through the end of 2022 and further increases in company earnings are expected. But it does seem that the momentum of growth is inevitably reducing, after its initial V shaped recovery.

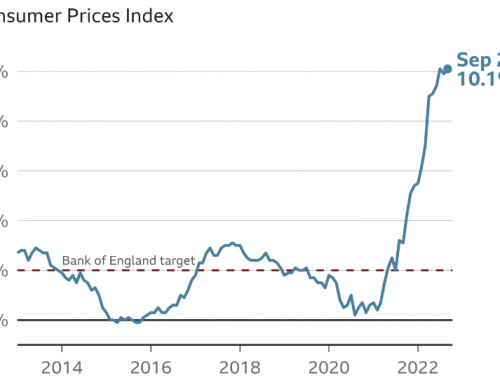

On the negative side, the Central Banks are looking to gradually withdraw from their massive quantitative easing programmes, which they will try to do without too large an impact on economic growth. Already the European Central Bank has announced a “recalibration” of the pandemic emergency purchase programme, which will see monthly purchases of bonds fall from 80bn euros to 60-70bn euros per month. The Committee is alert to the likelihood of a rise in volatility associated with uncertainties surrounding possible US Fed tapering and rises in short term interest rates. In addition, supply constraints are everywhere, which is leading to higher prices, particularly in materials, gas and oil prices. Although Central Banks opine that these rises in inflation may be temporary (and we note that they have a vested interest in having inflation to reduce the monetary value of accumulated government debts), markets and consumers are not yet convinced of this. Indeed, although Central Banks do not want to raise interest rates in case there is a negative impact on economic growth, the strong inflation numbers may at some point force their hands. Over the last quarter the risks of inflation have increased.

Q4 Outlook

In the short and medium term, equities look cheap relative to bonds and are, in our view, likely to outperform bonds but we are more nervous than we have been previously and have therefore made a small switch from equities into cash at our October review. This recognises the near-term uncertainty over supply shortages, increasing inflation risks and potential adverse impact on interest rates. The fact is that the world has created massive amounts of debt and is used to living in an environment where interest rates are negligible. Bond yields have risen recently but there is a long way for them to go if, as is looking increasingly likely, the inflation risks materialise. We know debt in many of the major economies is now over 300% of GDP; which may not be a problem whilst interest rates are low but any inflation-driven rises in interest rates will quickly create a funding problem. Meanwhile, many consumers (and voters) now feel that all problems can be solved by governments just spending huge sums of money. Eventually debt will have to come down, but will its impact be reduced by inflation, or by taxation, or by spending constraints?

Finally, a word on property, which is usually a good inflation hedge but, we feel, not from current valuation levels and we maintain a neutral stance on property.