It has been a volatile start to the year for risk assets. Russia’s invasion of Ukraine in late February shocked the world and is having a significant humanitarian impact. There are economic and financial implications too, and markets reacted as investors assessed the potential economic impact of sanctions on Russia.

Year-to-date, the FTSE All Share Index is down 0.8% (as of 28th February). In the US the S&P 500 Index fell 8%. European equities, represented by the Euro Stoxx 50 Index, fell 8.6%. Europe has a significant reliance on Russian energy, especially gas, and the invasion caused energy prices to spike higher. Emerging market (EM) equities recorded a negative return of 4.1%, represented by the MSCI Emerging Market Index, as markets priced in more interest rates increases by the US Federal Reserve.

In fixed income, there has been significant volatility as markets begin to absorb the enormity of the Ukraine situation. Corporate bonds have had a difficult start to the year, registering negative total returns (Europe in particular) as spreads widened. The spread is the difference between the yield on a corporate bond and a government bond. US corporate bonds performed relatively well, notably high yield where there was modest spread tightening in some sectors, including energy. Commodities have had a positive start to the year as Brent Crude oil prices jumped to more than $139 a barrel for the first time since 2008.

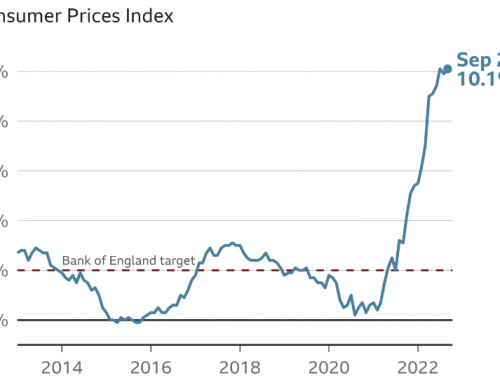

The pace of economic growth is now declining. Concerns about the Covid pandemic have subsided thanks to successful vaccine rollouts and a gradual re-opening of many economies. However, the gradual return to normality has fuelled increased demand for goods and services around the world. This is happening at a time when global supply chains are still struggling with Covid-related holdups and production constraints, especially in the energy sector. This has led to higher price inflation. For example in January, UK CPI inflation reached 5.5% year-on-year—its highest level for 30 years. And in the US, CPI hit 7.5% year-on-year.

Inflation has been mentioned at every turn since the onset of the pandemic. Nonetheless, consumers are used to small, incremental upticks in the cost of staples (food, clothing and other items). So the recent surge in energy bills and petrol prices has come as a shock to many consumers. The outcome is that consumers generally will have lower levels of disposable income and the rate of economic growth is likely to decline further.

Central bank policy and geopolitics are key risks that investors will be watching closely. US Federal Reserve Chair Jerome Powell’s comments at the end of 2021 and the beginning of the year indicated the US central bank would consider all options for the future path of policy. At the FOMC meeting in March 2022, US Federal Reserve officials sharply revised up their projections for interest rates this year compared to 3 months ago and they now expect six further increases this year (in addition to the March move) and three more increases in 2023. This would bring the US Fed funds rate to 2.8%. The European Central Bank announced it would scale back its own quantitative easing programmes at the end of March 2022. Monetary policy tightening impacts global financial markets because when interest rates are higher, this increases the rate at which companies future cash flows are discounted. This results in lower valuations for equities.

Outlook

Looking ahead, we think it is important to remember the path of economic activity prior to Russia invading Ukraine. The global economy was on track to accelerate sharply on re-opening and a recovery in the service sector. The key change is that higher energy prices and less disposable income for consumers, compounded by central banks raising interest rates means the risk of stagflation (slowing growth and higher inflation) has become more pronounced.

The war between Russia and Ukraine will remain a key factor in short-term market movements. The US and Eurozone economies had solid foundations prior to the war in Ukraine, however the surge in energy prices will generate some drag, especially in Europe. If there is a resolution to the Russia-Ukraine war, the focus of investors will return to inflation – which was the primary risk factor that was driving global markets (and central banks) prior to the war.