Market review

Equities and bonds delivered positive returns in Q1. World equities were up 4.3% and global bonds rose 3.0%. Most of the rise in equities came in January following stronger than expected economic data. More recently, bonds have rallied as expectations for future interest rates have fallen.

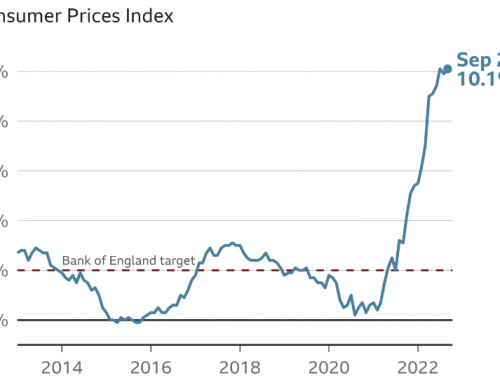

Inflation: Data releases in Q1 showed a trend of falling headline inflation in both the US and Europe, but core inflation, which strips out volatile inputs such as energy and is the focus of central banks, has not fallen and remains too high. Central banks’ ‘views’ on how to tame inflation remain the core theme for investors.

Interest rates: Central banks need to strike a balance between financial stability and price stability. Following the collapse of Silicon Valley Bank and UBS’s takeover of Credit Suisse, investors have reassessed their expectations for future interest rates. This led to a sharp drop in the yield of US government 2-year bonds. Prior to recent concerns about the financial sector, the market expected that central banks would continue to raise interest rates; now the consensus is that rates have peaked, and rate cuts are coming by year-end.

Outlook

We don’t see major direct economic impacts from the banking crisis. The main impact will be stricter lending standards. US and European consumers still have sizeable pools of excess household savings to support consumption. Our view is that we’ll see low or no economic growth in developed economies during 2023, offset by stronger growth in Asia.

We have not reduced equity exposure. We think equities continue to offer long-term appeal, particularly in an environment of stubborn inflation. We see value in Asia and Emerging Market equities and, in the US, we have more in smaller company equities.

Monetary policy works with a lag and the rapid increase in interest rates is unearthing cracks. Concerns over credit risk and over-leveraged assets have reinforced our view of investing more in higher quality bonds. We hold more bonds rated BBB or above (commonly known as “investment grade”) and continue to hold less in high yield bonds.

The interest rates paid on cash have introduced an alternative to equities and bonds. Variance across company performance is creating compelling opportunities for stock pickers. Recent strong performance from some of the active equity managers signals there are opportunities.