2020 ended with a positive quarter for equities and a negative time for fixed interest instruments. Overall, this theme continued into Q1 2021. In the UK, the FTSE 100 rose by 5.0% in the first quarter. Global equities rose by 3.8% in sterling terms, with the US S&P 500 up by 5.2%; Europe ex UK up by 2.5%; Emerging Markets added 1.9% and Japan TOPIX was up by 1.2%.

However, one of the significant market changes in the first quarter was the rise in the yields of longer dated government bonds. At the beginning of the year, the US Treasury yields were below 1%, but during the quarter began to move up to the 1.75% level. Similarly, UK 10-year Gilts started out on around 0.2% yields but rose to the 0.9% level. These rising yields saw corresponding falls in fixed income prices in Q1. UK Gilts lost 7.2%; UK Indexed Linked fell by 6.3% and UK Corporates lost 4.4%.

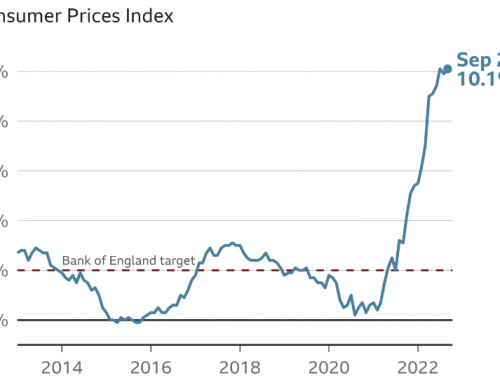

There are two main reasons for this. Firstly, the supply of government bonds has seen a massive increase in 2020, including the US announcing the addition of a further $1.9 trillion fiscal stimulus, with the follow up of a $2 trillion promise for infrastructure spending. The second reason relates to concerns about the likelihood of rising inflation, given the massive increases in global money supply and the various stimulus packages.

This concern has already been reflected in a rise in commodity prices in the quarter.

Industrial metals showed strong increases, led by gains in aluminium and copper prices. Shipping costs, having been in the doldrums, have also begun to rise as global demand begins to recover. Despite falling towards the end of the quarter, oil prices rose 22.4% in Q1 to $64. If we add to these increased costs, the increase in demand from the liquidity being pumped into the global economies, there is a definite risk of future higher prices. This risk may be higher in the US, where the stimulus has been higher than elsewhere.

In the UK, after all the previous talk and worry about Brexit, the coronavirus discussions have smothered any news on this front. In fact, apart from some initial transport issues with France in January, any negative consequences of the Brexit trade deal have not so far been obvious. The one exception to this is the trade between Ireland and Northern Ireland. Because of the success of the vaccine programme in the UK, the UK economy is likely to recover and grow much quicker than its European neighbours; many of whom are well behind in their vaccine programmes and in some cases still in lockdown.

On the International front, relationships appear to be becoming more uncertain and generally more dangerous. Russia has been making threatening gestures towards Ukraine; Israel has apparently attacked Iran’s nuclear plants and China is upsetting or putting pressure on India, Taiwan, and Japan.

Going forward we continue to see equities outperforming fixed income securities, particularly as the stimulus packages continue to work through the various economies and we are happy to hold our overweight position in UK equites and Emerging market equities but the Investment Committee remains alert to any build up in complacency surrounding the recovery in the real economy as reflected in the rebound in Equity markets.